Our glossary explains all the key terms surrounding guarantor loan products including costs, fees, applications, payments and collections. For any further questions, please read our blog or feel free to email us.

Affordability Check: During the approval process, the lender will review your affordability which checks whether or not you can ‘afford’ the loan. This includes checking your salary and expenses via payslips and bank statements and using this the lender can decide to match what you have asked to borrow, increase or decrease the requested amount or decline your application.

APR: This is the most common way to measure the cost of a loan or financial product across the world. Expressed as a percentage, it is the annual percentage rate as if the loan was taken out for a year and includes all fees in the calculation. For guarantor loans, the typical APR is around 39.9% to 49.9%

Arrears: When a borrower has missed repayments and is behind on what they owe to the lender, it is known as being in a state of arrears.

Bank Transfer: This is how the funds are transferred from the lender to the customer. For guarantor products, it is not usually through cash or cheque but sent electronically via bank transfer to the customer’s debit account.

Collection: This is the term used to describe a repayment from the borrower to the lender. For this type of product, you will usually repay in equal monthly instalments ranging from 12 months to 60 months.

Cooling Period: When a loan is successfully approved, the funds are sent to the guarantor first as a security check and also because they will be given a two week ‘cooling period’ where they can decide to forward the funds to the main borrower or send it back to the lender without being charged anything extra.

Continuous Payment Authority: This is the system used to collect recurring payments from a borrower. Rather than the customer having to make a manual payment each month, they will authorise their debit account and the collection will be made automatically on a scheduled repayment date every month. Read more about continuous payment authority.

Credit Check: This is a check carried out by the lender prior to approving a loan. It reviews the credit history of the borrower and the guarantor to get an idea of how well they have repaid other types of credit and loans in the past and whether they have any other payments outstanding. The lenders use this information to assess their creditworthiness and make a loan decision on this basis.

Default: When a customer misses a repayment and their balance is unpaid, it is known as a default.

Direct Debit: Also known as a ‘standing order,’ an individual is able to set up regular repayments with another individual or company using their debit card. With a direct debit, the card holder can choose how much they wish to pay and how often. It is a smart way to automate repayments coming out of your bank account and you have the option to cancel it at any point.

Drawdown: This is the loan amount that you borrow. When a lender issues you with a £5,000 drawdown, they are giving you a loan of this amount.

Early Repayment: All the guarantor lenders we feature on our website allow you to repay your loan early. So although you agreed to borrow the loan for 5 years, you may find that after 2 years, you are able clear your account. So you can simply call up or log into the account section of the lender’s website and pay it off. There may be some additional fees for repaying early if it is before a minimum threshold date, otherwise you will typically save money for having the loan open for less time.

Esign: Borrowers and their guarantors will always be required to sign an agreement during the application process which confirms the terms and responsibilities of the loan. Rather than having to print off, sign and post back the contract, applicants are able to electronically sign the loan agreement using a pin code sent to their phone and verification link in their email – saving them time and speeding up the process.

FCA: This is the Financial Conduct Authority that is responsible for regulating the guarantor loan industry. Our website is an authorised credit broker of the FCA.

Fixed Interest: This is where the interest charged on the loan remains fixed and stays the same during the loan term. The majority of guarantor lenders offer a fixed interest rate with only a few stating this might change during the loan term, known as a variable interest rate.

Guarantor: This is the person that agrees to guarantee repayment on behalf of the borrower. So if the main customer cannot keep up with their repayments, the guarantor can step in and make payments on their behalf. It is usually a close family member such as a parent, sibling or spouse or possible a close friend.

Guarantor Loan: A customer can borrow up to £15,000 provided that they have an extra person to ‘guarantee’ the loan and repay if they cannot keep up with the repayments.

Homeowner: This is a person who owns a home either outright or with a mortgage. Some guarantor loan companies require the guarantor to be a homeowner, because having a property provides extra security that the person will not leave their home or can potentially release equity from their home to help make repayment.

Loan Amount: This is the amount you are looking to borrow with guarantor providers offering loans ranging from £500 to £15,000 depending on your credit score, affordability and other measures.

Lump Sum: This is a single payment of money so when your loan is approved, you receive the entire amount you asked to borrow in one lump sum. This is different to some loans where the money is staged and released in bits.

Representative APR: This is the rate advertised by lenders and will be offered to at least 51% of successful applicants that are funded for a loan. The amount charged will vary based on their credit score, affordability and duration of their loan.

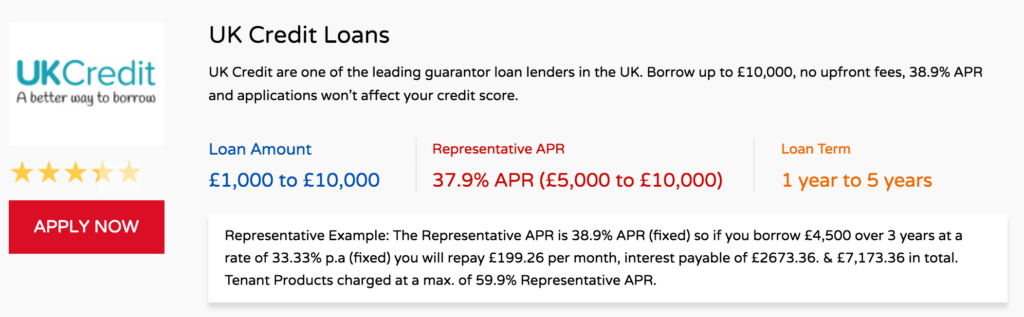

Representative Example: The amount that the customer will be charged, but again, for at least 51% of customers. It gives potential applicants an idea of how their loan works and how the repayments are broken down. See an example from UK Credit below:

SECCI: This is a key part of the loan agreement that you sign prior to receiving your loan. It stands for the Standard European Consumer Credit Information and highlights the terms and conditions of your loan.

Tenant: There are specific tenant guarantor loans where the lender does not require your guarantor to be a homeowner. So you are able to be approved for a loan even if your guarantor lives in rented accommodation, provided that they have a good income and credit history.

Treating Customers Fairly: This is a requirement of the FCA and is the notion, culture and procedures of a company to treat customers in the best interests, providing them with transparent information and doing what is best for the customer.

Typical APR: The rate of interest charged to at least 66% of customers that are successfully funded, however, most lenders in this industry use ‘representative APR.’

Underwriting: This is the stage of the application process where you are being reviewed by the lender and they are making a decision on whether to approve your loan or not. It is common to say that your ‘loan is in underwriting.’

Variable Interest: This is where the interest that is charged by the lender changes during the loan term. With some loans lasting as long as 7 years, this is the chance that the rate they will charge you will increase or decrease. Amigo loans state that they have a variable interest rate however, it has never been changed during a customer’s loan.